The new tariffs are illegal, but for a different reason

Raymond James Chief Economist Eugenio J. Alemán discusses current economic conditions.

As we have said several times before, we are not lawyers, we are economists, so this section title doesn’t mean that we actually know what the courts are going to conclude about these new tariffs, but we will make our argument on the basis of economic analysis. If the courts follow the economics of the argument, then the only way they can rule is against the tariffs.

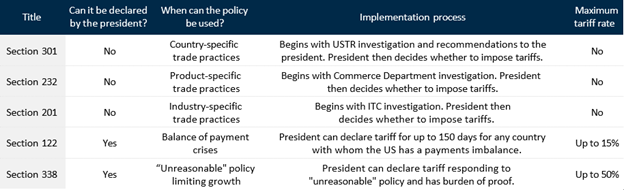

First, and this is important, we have to clarify that we think the administration is using these tariffs to buy time to figure out what to do next. The president has legal authorization to impose a tariff rate of up to 15% for 150 days. Since courts will probably take more than 150 days to declare them illegal, then it is probably smooth sailing for the administration during this period. After that, other, more complicated avenues need to be followed, but we will discuss them at the proper time.

The decision by the Trump administration for basing tariffs on the International Emergency Economic Powers Act (IEEPA) had a fundamentally legal twist to it. Courts needed to figure out if IEEPA gave the executive branch authorization to impose tariffs, which is a taxing power constitutionally reserved for Congress, that aims at increasing tax revenues.

Since only Congress has the power to impose taxes - in this case, as tariffs - then the court simply ruled on whether IEEPA gave the president, any president, the authorization to impose tariffs using IEEPA.

Of course, the administration, in an attempt to change the narrative, has been saying that “tariffs are paid by the exporting country and not by Americans.” If the administration had convinced the Supreme Court that tariffs were paid by foreigners and not Americans, then the Court may have concluded that tariffs could potentially be implemented using IEEPA.

However, economic theory and evidence from economic research have concluded, in this case and in historical cases, that tariffs are a tax on individuals and firms of the importing country, i.e., the United States in this case. This is the reason betting markets had estimated that the administration was going to lose its case in the Supreme Court. Thus, the Court concluded that IEEPA did not authorize a US president to raise taxes, in this case in the form of tariffs.

After the decision from the Supreme Court, President Trump doubled down and imposed a 10% global tariff under Section 122 of the Trade Act of 1974. As we said above, Section 122 gives the president authority to impose tariffs of up to 15% on a temporary basis. The duration of this period is 150 days.

However, the Trade Act of 1974 gave this authority to the president if the country was facing a “balance of payments crisis.” What is a balance of payments crisis?

Is the US experiencing a balance of payments crisis? A balance of payments crises is a situation where capital flows out of the country so rapidly, and so massively, that it triggers a large depreciation of a country’s currency. If a country suffers a balance of payments crisis, the country may not be able to pay for imports and/or could lose international reserves, threatening its ability to pay its debt obligations.

Let’s take each one of these arguments one by one.

There is no reason why the US may not be able to pay for imports because imports are paid in US dollars and the US has the ability to print as many US dollars as it wants. So, the question is, why did the US Congress pass the Trade Act of 1974? Because the US used to have a fixed exchange rate, and under a fixed exchange rate system, this could have been an issue if the US government wanted to keep that fixed exchange rate system in place.

Today, however, the US has a flexible exchange rate, which works as a shock absorber for the economy whenever there is a shock. By the way, the US dollar came out of a fixed exchange rate regime during the period of 1971 to 1973, under President Nixon. Thus, when the US Congress finally passed the Trade Act of 1974, the balance of payments argument was already obsolete.

The second argument, that a country could run out of currency reserves and not be able to pay its debt or interest payments on its debt, only applies to countries that suffer what some have called the “original sin.” This means that if a country borrowed in US dollars, but its fiscal revenues are denominated in the domestic currency, then a large depreciation of the domestic currency will lead to the country being unable to pay its debt service payments, which are denominated in US dollars. Thus, after a balance of payments crisis, a large devaluation of the domestic currency leads to a debt default.

What is even more interesting about Section 122 is that the Trump administration’s own lawyers argued, during the legal process that ended with the Supreme Court decision against IEEPA, that using Section 122 from the Trade Act of 1974 to impose tariffs was not feasible because there was no balance of payments crisis in the US.

The bottom line is that we had estimated that tariff uncertainty was going to diminish this year. However, this new environment is throwing another wrench into the road to firms’ decision making, which could hurt economic growth. For now, investment in AI as well as the effects of higher wealth are keeping the economy strong. However, the reaction of firms to these new levels of uncertainty will remain a challenge, especially for employment growth.

Economic and market conditions are subject to change.

Opinions are those of Investment Strategy and not necessarily those of Raymond James and are subject to change without notice. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. There is no assurance any of the trends mentioned will continue or forecasts will occur. Past performance may not be indicative of future results.